Canadian businesses and consumers increasingly expect real-time payment experiences that take the friction out of their online transactions.

At a time when Canada’s productivity growth is lagging behind that of its peers according to some measures, there is increasing evidence that the advancement of faster, more seamless payments and financial innovations can spur economic growth and competitiveness.

When it comes to the payment processing needs of Canadian enterprises, some of the pain points are quantifiable: Traditional payment methods (such as cheques and electronic funds transfers [EFTs]) cost Canadian businesses an estimated $2.9 to $6.5 billion annually due to inefficient, labour-intensive processing, difficulty tracking payments and limited visibility into cash flow. An Interac survey from 2018 found that 46 per cent of business decision makers find reconciling payments to be time-consuming, and a roughly equal amount (45 per cent) acknowledged that many payment processing activities can be tedious. A recent C.D. Howe report estimated the Canadian economy will see $3.24-billion in efficiency gains from real-time clearing and settlement of payments over the first five years after it is introduced. In short, cheques and EFTs are too slow and inconvenient for 21st-century Canada.

Canada is ready for payments evolution. Players in the ecosystem have already begun to unlock the benefits of modernized payments and digital innovation more broadly — with further reforms on the horizon including real-time settlement and open banking.

Here’s a look at the latest Canadian payments (and payments-adjacent) advances, and what we can anticipate over the next few years.

Payments and related technologies: An evolving picture

Real-time payments

Faster digital payments give businesses advantages over traditional payment methods. They provide increased transparency around data and cash flow, helping to create a clearer picture of a company’s payables and receivables in real-time.

Canadian businesses are understandably keen to take advantage of these features to address critical needs and challenges, for example by phasing out cheques in favour of digital payment methods (as nearly three-quarters of businesses surveyed by Interac plan to do over the next five years).

To continue to compete in a fast-paced, global economy, Payments Canada is modernizing Canada’s national payments infrastructure, which includes the Real-Time Rail (RTR), a real-time payment system that will enable faster, data-rich payments. As the exchange vendor of the RTR, Interac successfully completed the components that will allow for the exchange of real-time payment messages in June 2023. In April 2024, Interac shared that it is exploring a centralized fraud and directory service with Payments Canada, drawing on our proven expertise and delivery track record as a trusted connection point for faster digital payments.

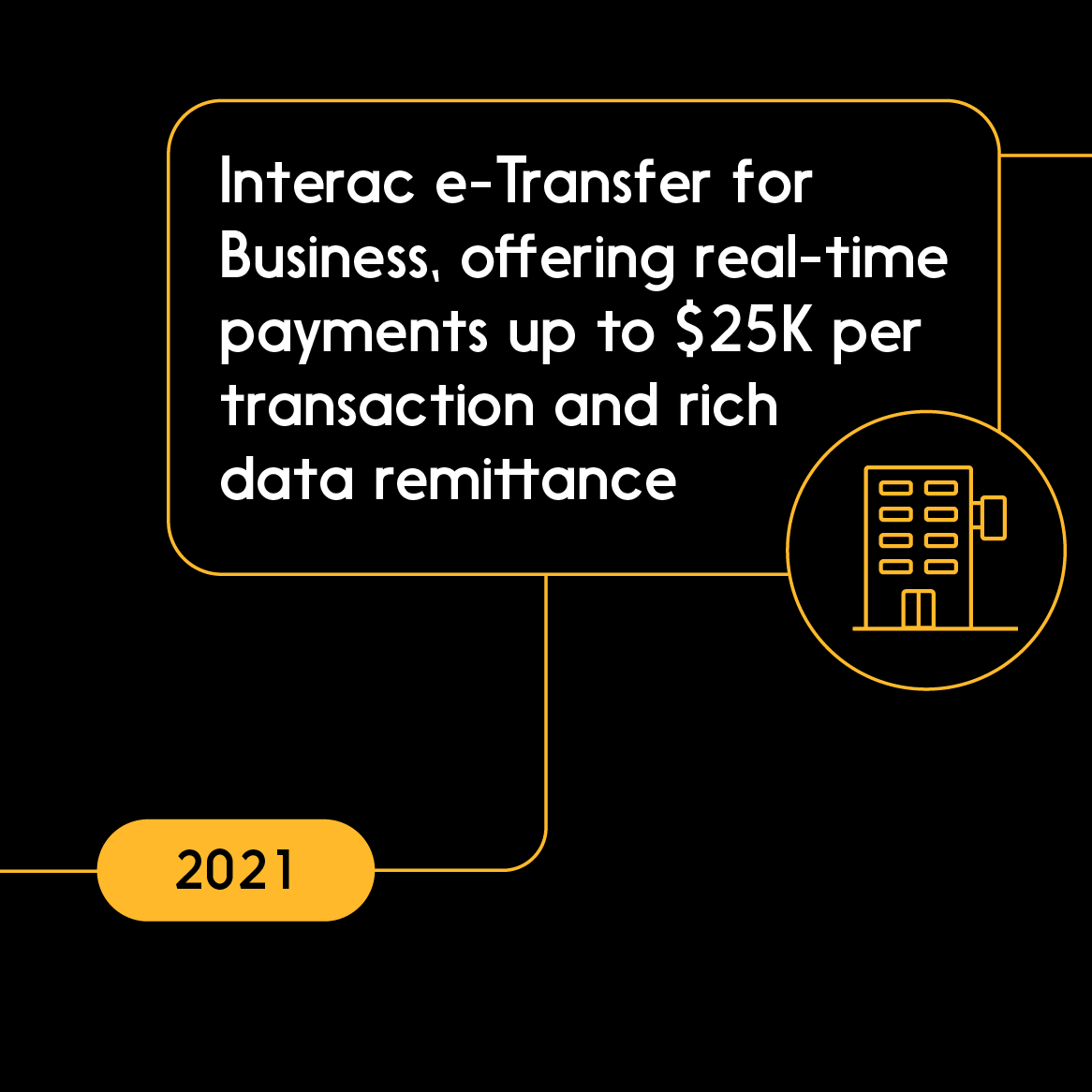

Interac e-Transfer for Business is a solution that organizations can take advantage of now. Launched in 2021 in response to the needs of Canadian businesses, Interac e-Transfer for Business allows users to send payments of up to $25,000 per transaction (depending on the financial institution, which sets the limit). The service is ISO 20022 compliant, which enables interoperability and integration between ERP systems and accounting applications. For organizations that take advantage, that means fewer person-hours dedicated to processing invoices and payments, freeing up resources for more strategic activities (something 77 per cent of finance professionals polled told Interac they want).

Just like businesses, consumers appreciate getting paid quickly. In Canada, they’ve already been enjoying fast account-to-account money transfers for two decades thanks to the Interac e-Transfer service.

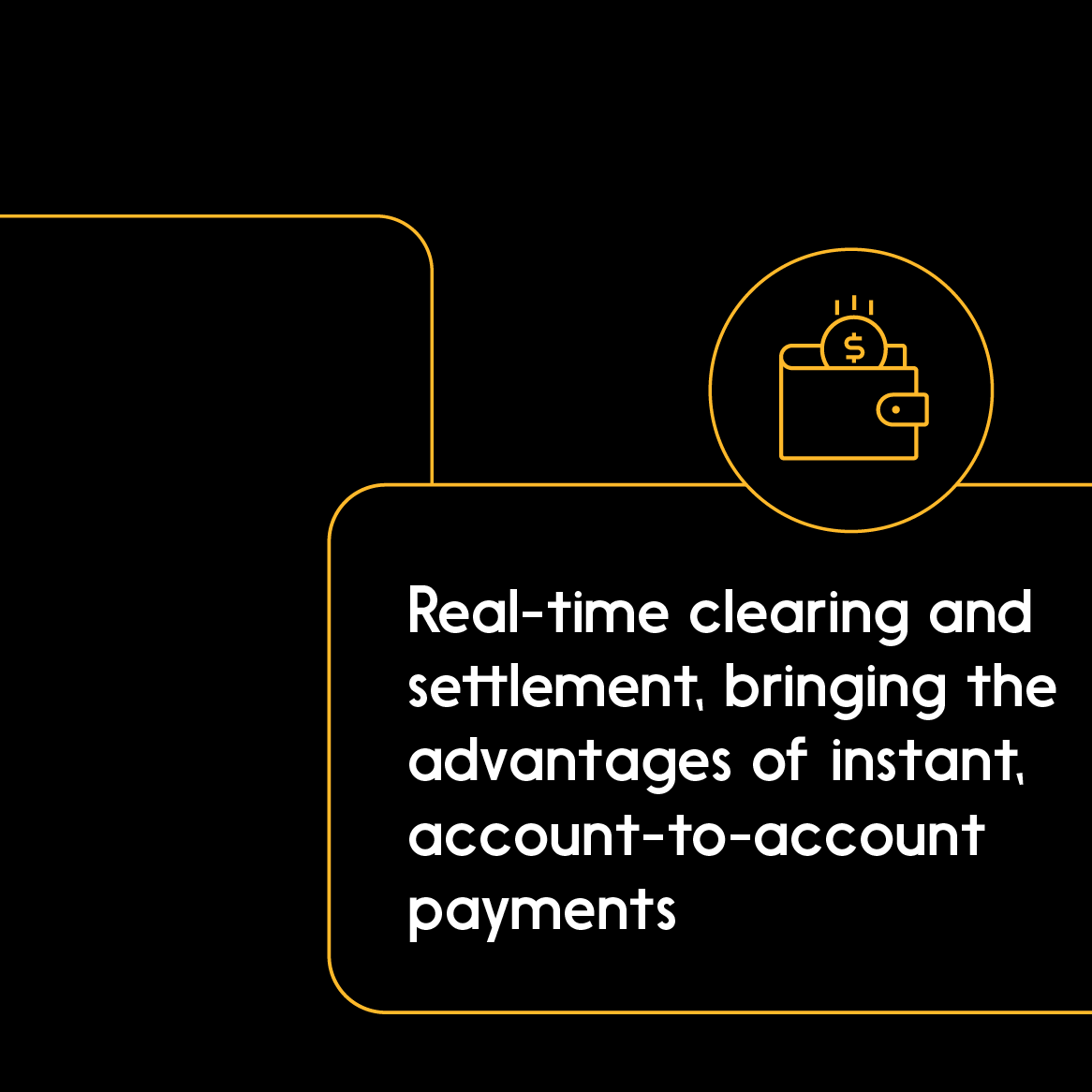

In other words, Canadians already have access to the kinds of benefits that faster payments systems have brought to other markets around the world. What’s left to accomplish is the establishment of real-time clearing and settlement, which will provide meaningful improvements for businesses and consumers including immediate availability of funds if someone pays them by cheque or EFT, payroll efficiencies and more.

Expanding the reach of Interac Debit

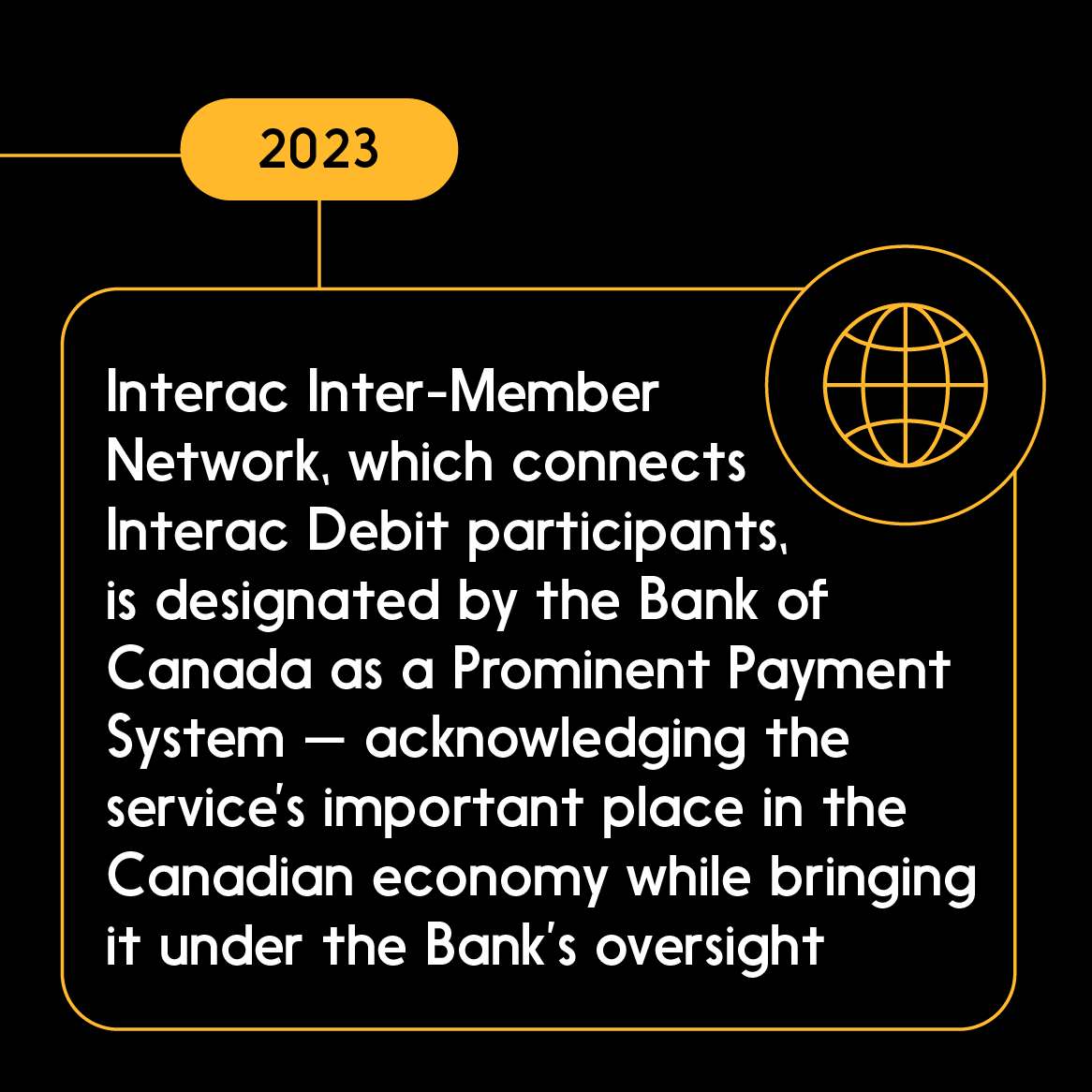

Interac Debit is essential for commerce in Canada. Not only is it a near-ubiquitous payment method among Canadians (the service recorded 6.2 billion transactions in 2022), it’s also one that people without credit can conveniently use for digital transactions.

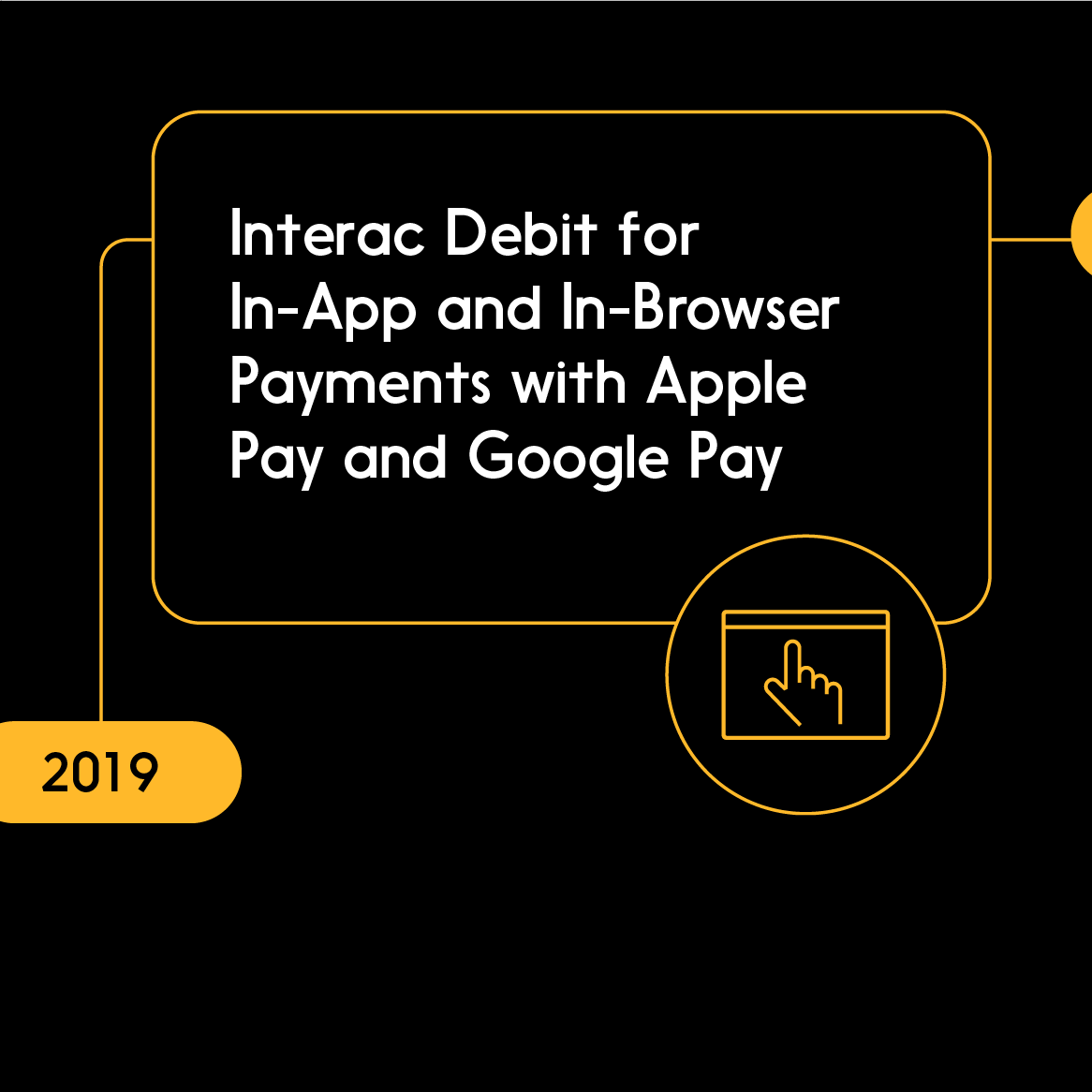

The work of introducing the convenience of InteracDebit to more use cases and contexts continues. For example, InteracDebit is available as a contactless payment method for adult fares on select transit systems across Canada, enabling riders to tap and go on a fare reader with their debit card or mobile device, with no need to carry a specialized fare card or tickets. Since 2019, Canadian consumers have also enjoyed access to InteracDebit for In-App and In-Browser Payments with Apple Pay and Google Pay, and they’re taking advantage: InteracDebit In-App transactions grew 17.5 per cent year-over-year in the 12 months ending July 2023.

Also in summer 2023, Interac announced that Interac Debit for mobile contactless payments reached the milestone of one billion transactions in a 12-month period. for the first time, driven by the preference of Gen Z adults to pay using their smartphone rather than a physical wallet and cards.

And as of 2024, accepting payments directly on a compatible mobile device offers merchants a convenient, affordable, and secure way to accept all types of contactless payments on the go—no additional hardware or payment terminals required. By accepting Interac Debit payments directly on a smartphone or using a card reader for a smartphone or tablet, businesses can provide their customers with a fast, seamless checkout experience.

More convenient point-of-sale payments with InteracDebit

As part of the overall shift toward faster digital transactions, small retailers and micro businesses need solutions for affordable and easy-to-use point-of-sale systems that offer convenience and flexibility.

And now, businesses of all sizes can accept contactless payments directly on a compatible mobile device. Accepting payments on mobile devices offers merchants a convenient, affordable, and secure way to accept contactless Interac Debit payments on the go—no additional hardware or payment terminals required. By accepting debit payments directly on a smartphone or using a card reader for a smartphone or tablet, businesses can provide their customers with a fast, seamless checkout experience.

Open banking

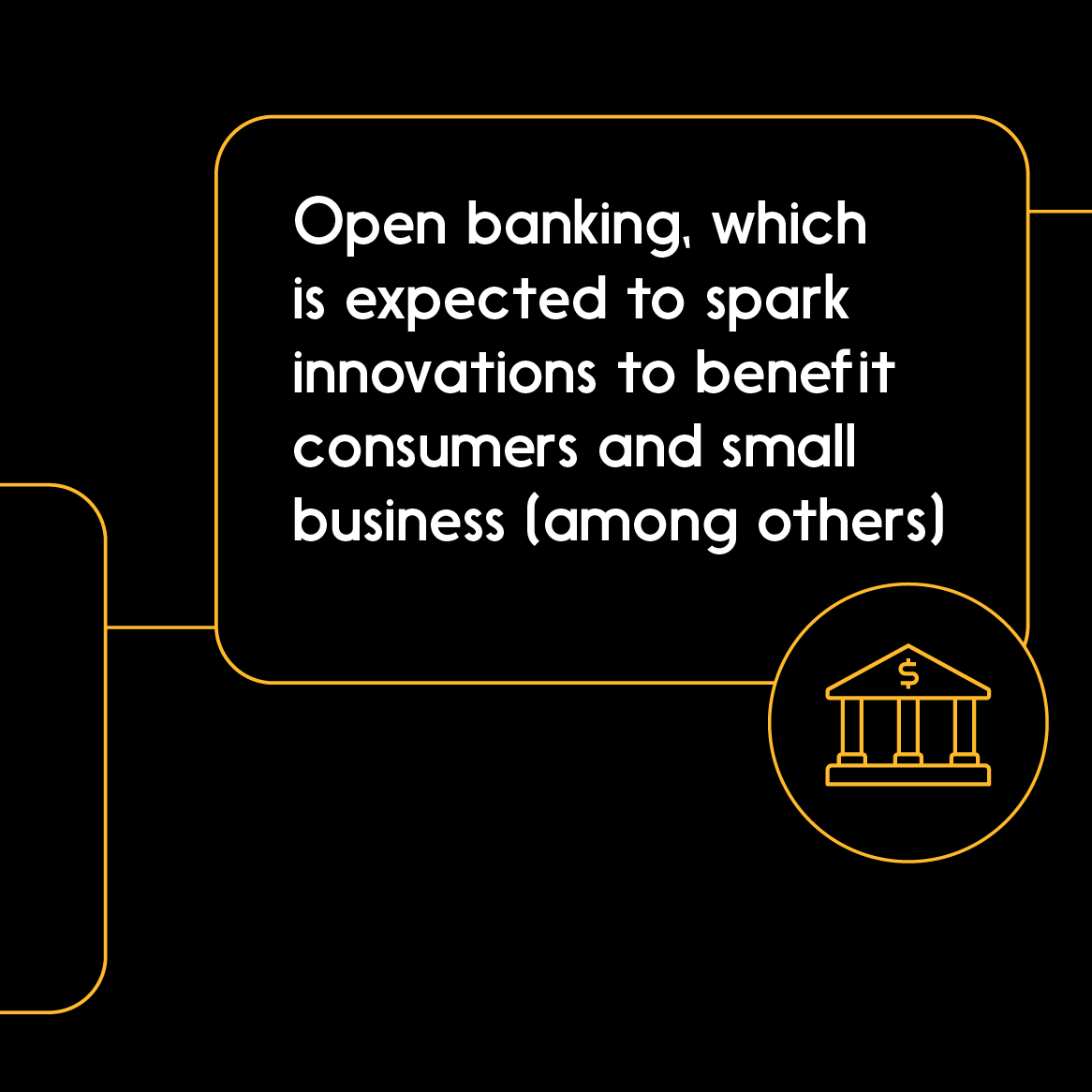

Canadian businesses that keep an eye on global payment trends may also be eager to see an open banking system take effect here — as has already happened in markets like the United Kingdom, Europe and Australia, where small businesses are reaping the rewards.

The Government of Canada is working to implement an open banking framework, based on the advice and input of industry and working groups which Interac participated in. The goals of this framework are to provide Canadians with the means to control and securely share their financial data to gain access to new products, services and innovations. Interac has focused on the importance of consumer consent within an open banking framework. We’ve also worked with ecosystem partners to create a minimum viable ecosystem testing ground for open banking concepts, which helps us understand other stakeholders’ needs and input.

Payments in Canada: The work continues

At Interac, we recognize that there’s more work to be done to modernize payment processing in Canada.

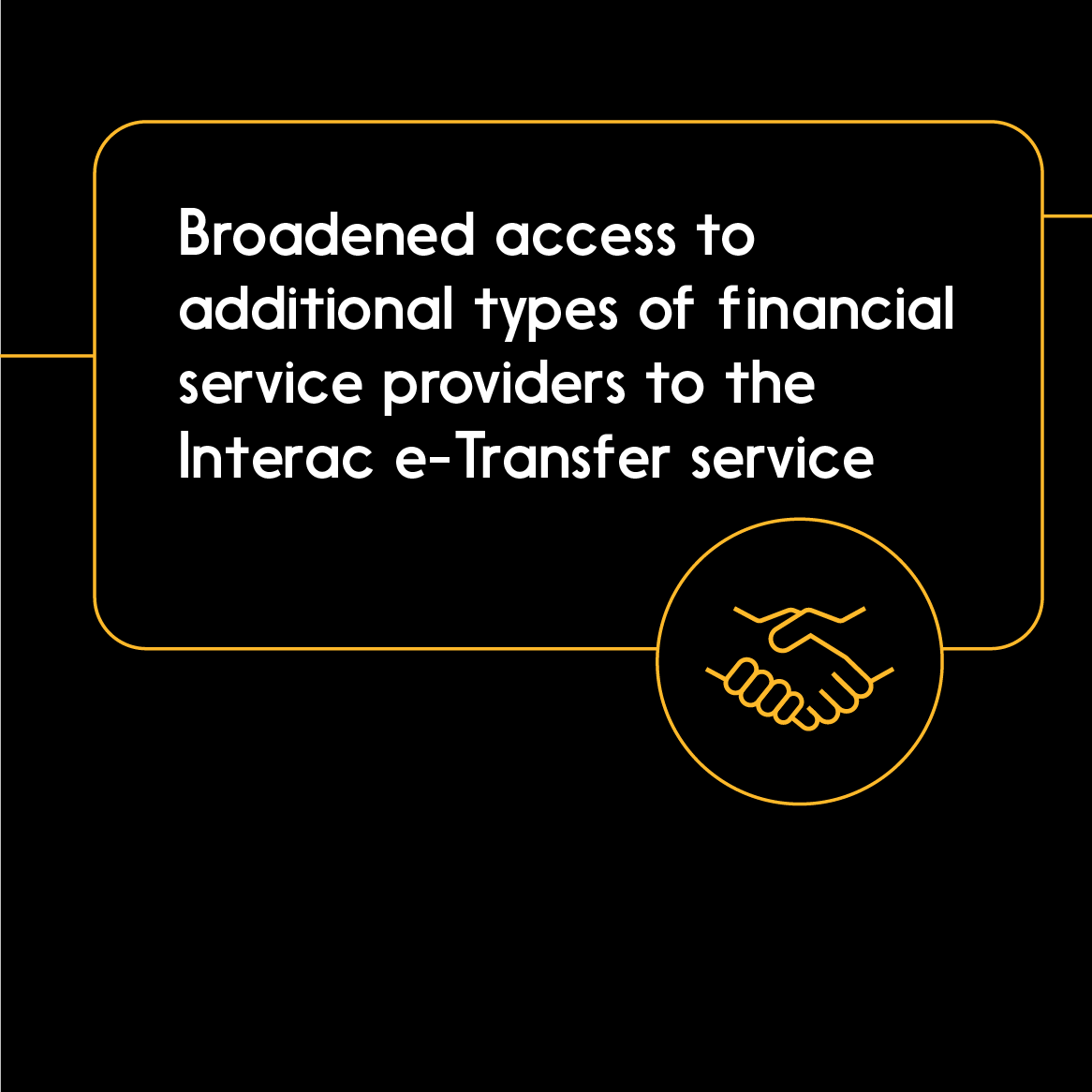

Broadening access is part of that work. Interac is expanding the availability of its network by broadening access to the Interac e-Transfer service to more financial service providers. Organizations may now apply if they are both FINTRAC-regulated Money Service Businesses (MSBs) and investment dealers regulated by the Canadian Investment Regulatory Organization (CIRO). Wealthsimple, a digital investment management service, became the first organization to receive provisional approval under this new criteria.

The federal government has also brought forward amendments to the Canadian Payments Act to expand membership eligibility in Payments Canada, which is expected to lower transaction costs and deliver “faster, more secure payments” for Canadians.

In short, this is an exciting time for payments in Canada. With so much change underway, we have a unique opportunity to make Canada’s digital economy more competitive, and deliver the benefits of secure, advanced payment technologies to every business and household in the country.

What other benefits is payments modernization bringing to Canada?

Apple, the Apple logo, and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries. Apple Pay and Touch ID are trademarks of Apple Inc.*

Google, Google Pay and the Google logo are trademarks of Google INC.**